Impact of Negative Real Salary Increases on Employees in Africa

Impact of Negative Real Salary Increases on Employees in Africa

Are your employees in some African countries moaning about salaries?

During the annual salary increase cycle, clients often question why inflation is such an important input when determining an equitable salary increase for employees. Inflation plays a crucial role due to its direct impact on the purchasing power of employees. And this is especially important in Africa where a sudden, and often dramatic, increase in inflation is experienced and/or where there is a high prevailing inflation rate.

Granting a negative real salary increase can have dire consequences for employees.

A real salary increase refers to an increase in the employee’s salary that exceeds the rate of inflation, resulting in a higher purchasing power for the individual. In other words, a real salary increase means that after accounting for inflation, the employee has more money to spend on goods and services than they did before the increase.

For example, let’s say you granted an employee a 5% salary increase. If the inflation rate is 2%, then the employee’s real salary increase is 3% (5% – 2% = 3%). This means that their purchasing power has effectively increased by 3% because their salary has grown faster than the prices of goods and services.

Concomitantly, if you grant a negative real salary increase, this results in negative purchasing power which can have several adverse consequences for employees. It can lead to a decrease in their standard of living, as the employee finds it increasingly difficult to afford the same level of goods and services as before. It may also result in financial stress, as employees struggle to make ends meet due to their diminished purchasing power.

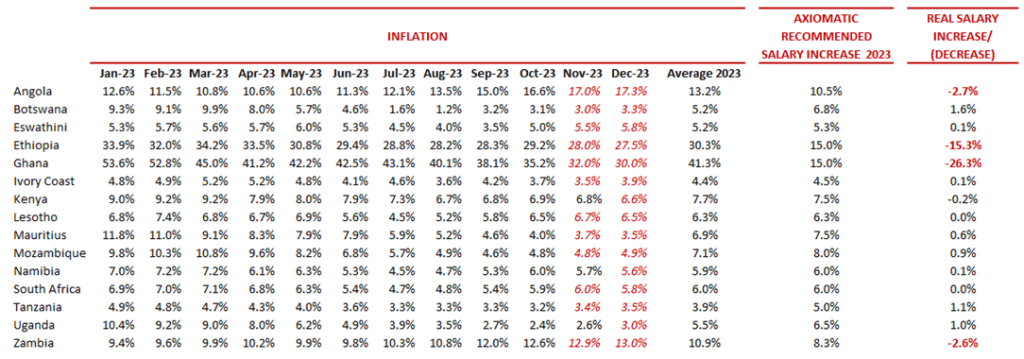

Having defined the problem and the consequences of granting a negative salary increase, it is worthwhile considering some African countries with high inflation rates.

What is now patently obvious, is that if you granted employees in the above countries a salary increases this year of less than the “Expected 2024 inflation” shown in the table above, they have received a negative real salary increase and concomitantly, they will experience a decline in their purchasing power.

Of course, other factors must also be considered which could mitigate the erosion of an employee’s purchasing power. However, these factors may also exacerbate the hardship.

For example, in Malawi, the tax tables were amended with effect from 1 April 2024 as detailed in the table below. In a high inflation environment, where we are projecting an average inflation rate of 25.5% for 2024, one would expect the tax bands increases to be correlated with inflation. Without adjusting income tax bands/ brackets and thresholds for inflation, taxpayers may find themselves pushed into higher tax brackets even though their real income hasn’t increased. This results in taxpayers paying a higher proportion of their income in taxes, effectively increasing their tax burden.

For employees earning above MWK 1,800,000, the higher limits will decrease the tax payable monthly and increase their net pay, but it will not compensate them for the erosion in their purchasing power which they will experience because of the high inflation rate and the possible negative salary increase.

While we are not saying that an employer should simply align a salary increase to the expected inflation rate, one must be cognisant of the erosion of employee’s purchasing power in some African countries. And perhaps most importantly, understand why they are moaning.

Impact of Negative Real Salary Increases on Employees in Africa Read More »